If you have ever wondered what your credit score is, you aren't alone. ZILLOWPOPULATIONSCIENCE states that the average American is only able to understand two things about credit scores. This gap is present across all age groups. Boomers and Generation X'ers knew less about credit than the Gen Z's. Continue reading to find the answers you need about credit scores.

Commonly asked questions about credit scores

Your credit score can make a big difference when applying for loans, apartments, and jobs. It's important to know what it is and what it means to you if you plan on reaching your financial goals. Credit scores are determined by several factors, including your credit utilization, payment history, and debt. Lenders also use your score to determine how likely you will be to repay future loans.

How do you find your score?

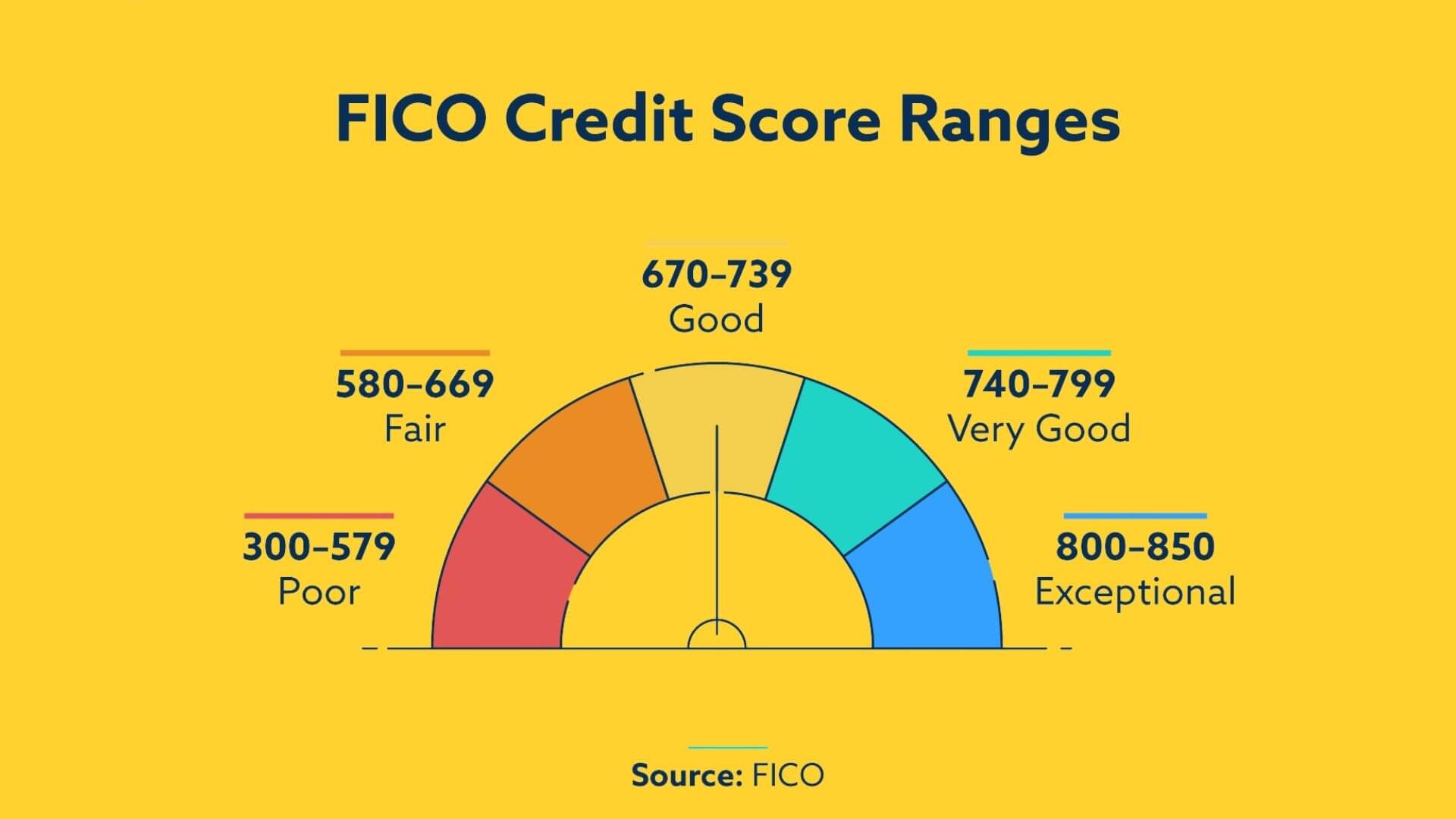

The credit score is the number that lenders use to determine whether you're a good risk for them to lend money to. It ranges from 300 to 850 and tells lenders whether you'll be able to repay loans. Credit history has a significant impact on your score so it is important to keep track.

Hard inquiry vs. Soft inquiry

There are two types if inquiries that you can make on your credit report: a hard inquiry or a soft inquiry. Both have different effects on your credit score. A hard inquiry occurs when you apply in person for a loan like a student loan, a car loan, or mortgage. Depending on your credit history, a hard inquiry may lower your credit score by 0-5 points. It is important not to apply for credit again if you do not need to.

Impact of hard inquiry upon your credit score

Hard inquiries are made on your credit reports when you apply for a loan. Hard inquiries tell potential lenders that your are looking for credit. This will hurt your score because it will appear on your report, regardless of whether the application is approved or rejected. Hard inquiries are also a sign that you have applied to credit in the past two year.

A good credit rating

It is essential to pay your bills on-time in order to maintain a good credit rating. You will have a negative impact on your credit score if you miss one or more payments. Credit score is more about how well you pay your bills. Automatic payments will help you avoid falling into the trap of forgetting your payment.

Before applying for a mortgage, you need to be aware of your credit rating

Before applying for a loan you should know your credit score. This can impact your application. This also gives you insight into your finances. Your credit score is used by lenders to help you determine your repayment patterns. Your credit score is just one piece of the equation. Your income is also taken into account by lenders, which could affect your score. By regularly checking your credit score, you can spot red flags and avoid being taken advantage of.