As long as you fulfill certain requirements, you can build credit at any age. Most of the main credit scoring companies, FICO and VantageScore, don't have an age requirement to qualify. It all depends on what score you have and your credit history. Credit scores don't start at zero. However, they can be calculated as a range starting at 300 (the lowest possible score), and moving up depending on the information in credit files.

Authorized user status allows your child credit building

The majority of credit card companies allow children to use their accounts as authorized users. They must be 13 years or older. Your child can be added to an account as an authorized users. This will help build their credit history and increase the rewards. This will help your child build their credit and make it easier to access money as they age.

It is a great way to help your child build credit history and credit scores. They will also have a history paying on time, which will help their credit rating. This will affect your credit history and the credit score of your child. A high credit score can be negatively affected by late payments and high balances.

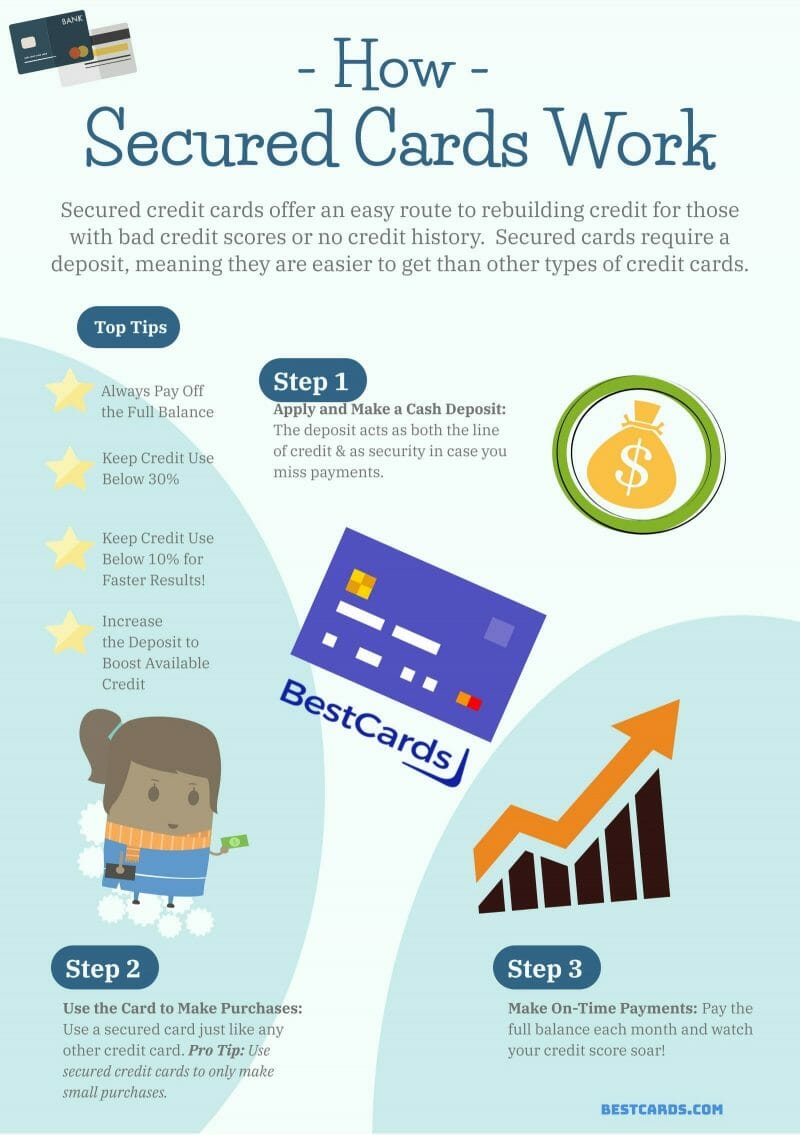

Secured credit is a good way for credit to be built

If you're new to the credit world, a secured credit card can be an excellent way to establish yourself. These cards don’t require any initial deposit. They also report your payments to the credit agencies regularly. These cards teach responsible spending habits and help build credit. Secured Cards are for those who don't have the credit skills to get a card.

Do your research before you apply for a secured credit card. You need to be aware of hidden costs and high fees that can come with these cards. Secured cards work best if they don’t have an annual fee, provide purchase protection, and keep track of your credit score. A secured card may offer cash back or rewards.

A secured card also has the added benefit that it is easier for you to apply. Secured cards can report your payments directly to each of the three credit bureaus. This improves your credit score. Your score will be affected if you don't pay your bills in time. You should also keep your credit balances low, under 30% CUR. If you follow these tips, you should see an increase in your credit score in a few months.

Co-signing is risky when you are trying to build credit.

Co-signing is risky for both co-signers as well as borrowers. It involves placing your personal credit in another person's hands and is not recommended for anyone under 21. Many young adults do this for student loans. Often, their parents co-sign in order to support the application.

A co-signer is a risky move that could damage your credit history and relationships. The lender will sell a cosigner's credit card to a debt collection agent if they are unable to pay their dues. In this case, the collector will go after the primary borrower and not the cosigner. A co-signer might file bankruptcy, which could affect their ability to pay their obligations.

You can add an authorized user to your credit card account if you aren't sure if co-signing is right for you. Although authorized users can help establish credit history and avoid the risk of co-signing with others, it is important to choose carefully who your authorized user will be. Make sure they can repay any charges made on the account.