We'll be discussing the FICO(r), score 9, and explaining what it all means. We'll also discuss MyFICO, other options for a FICO(r) Score, and how rent payments can affect your credit score. Let's begin by discussing the first three elements that affect your FICO score. You'll probably want to know what each one means to you, so read on.

FICO(r), Score 9

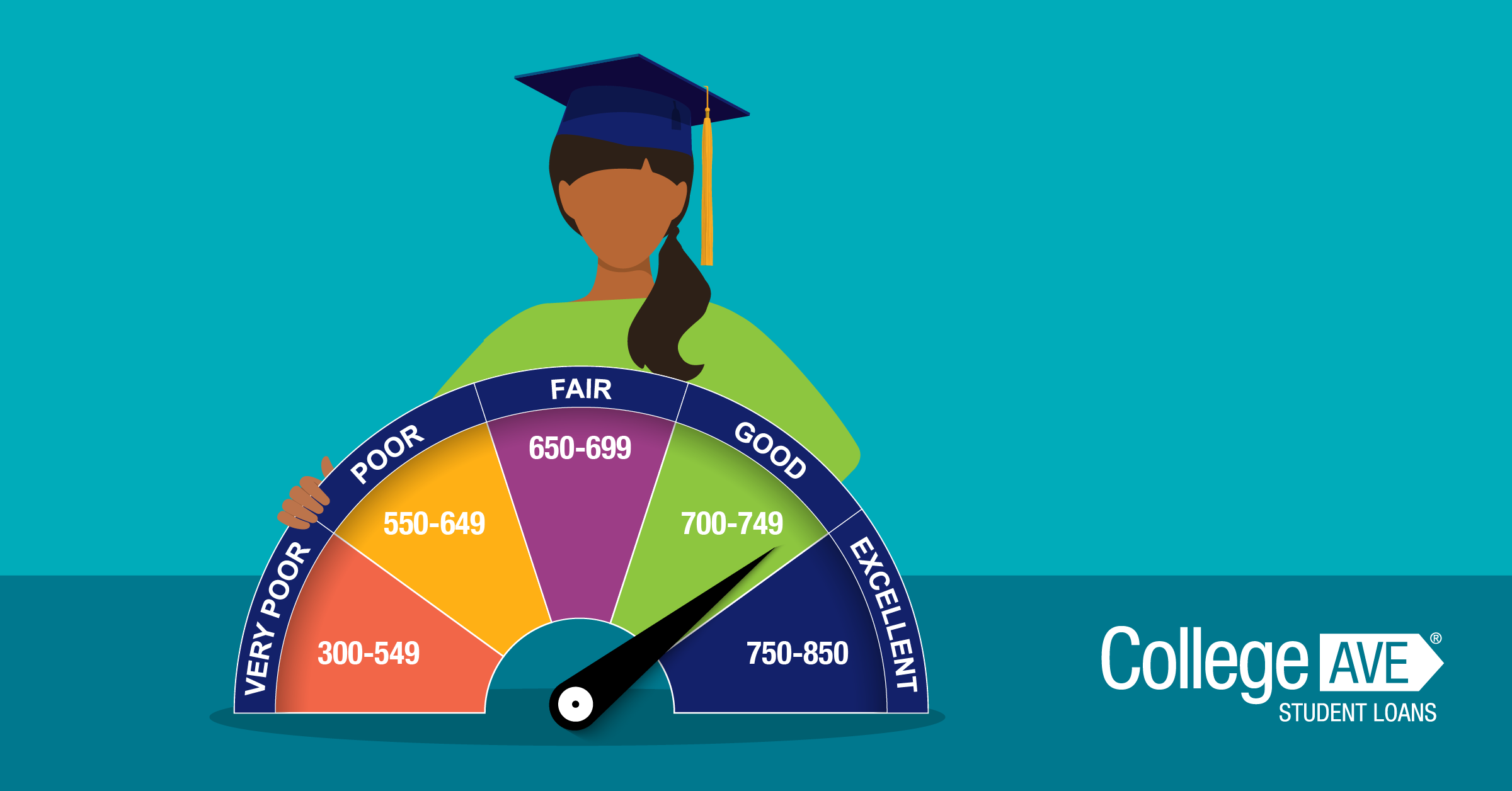

Although FICO(r), Scores have been around since over 25 years, they are still the most widely used and well-known. Lenders began using FICO (r) Scores for the first time in 1989. There have been many changes since 1989: consumer demand, data reporting practices, credit-granting requirements. Here's what to know about the credit scoring system. As always, remember to keep your score!

The FICO(r) Score 9 has several changes compared to its predecessors. You can no longer include medical debt in your score calculation. Therefore, if your score has been affected by a bill you received from a physician for surgery, it will be less than if your score was affected by a credit-card bill you received for the same procedure. Because collections do not affect your rental history you can start building credit history by paying rent.

Impact of rental payment history on your credit score

Although it might seem counterintuitive to think that rent payments can affect your credit score they actually do. Credit bureaus provide this information. Whether you've made on-time payments or missed them is one factor in the credit scoring process. Credit scoring models take into account both your rental history and overall credit history. You should still be aware of the important information about credit reporting data. Continue reading for more information.

Experian has found that 75% reported a credit score increase when they include rental payments in their credit report. That increase can range from 11 to 29 points. It may not seem like much but it will be a big help. Although the impact may not be immediate, it can make a significant difference in your credit score. Continue reading to learn more about the impact your rental payments history has on your credit score.

MyFICO

If you have a low credit score you might wonder what MyFICO score 9 is. Access it is free and easy to get from your credit card provider, lender or credit counselor. It is possible to have a poor credit report. If you dispute it, your score can be lower. Good news is that you can improve your score and maintain low interest rates. Listed below are some ways to do this.

Medical Collections: Unlike in previous FICO scores, medical debt isn't considered as a large factor in determining a credit score. According to the Consumer Finance Protection Bureau the impact of medical collection on credit scores is less than that of other types. You shouldn't ignore medical collections accounts completely. While the FICO formula will now take medical collections into consideration, it isn't clear how much. Because medical collection accounts aren't as important as other types, they won't have a negative impact on your score as negatively as other debts.

You can also get a FICO(r), Score.

FICO(r), has been around over 30 year. They are an easy measure of creditworthiness and are closely related to each other. The newer version is called FICO(r) 9, and it was designed to be more credit-friendly to consumers. It considers things like rental history and payment history. However, it makes them less detrimental. A FICO(r) score 9 can also be obtained through student loans, debt consolidation loans, and home equity loans.

Although FICO(r), 9 may not seem like much, there are still things you can do that will help improve your score. You can make your payments on-time, for example. Doing so will raise your FICO score to 25 points. For a small fee, LevelCredit will allow you to access 24 months of your past payments. Keep in mind that not all lenders are using the newer model yet, so you may need to wait a few months before getting your FICO score.